ILIT vs. Revocable Trust: Which Is Better for Your Estate?

- John McDonough

- Dec 30, 2025

- 3 min read

One of the most common questions in estate planning is whether an Irrevocable Life Insurance Trust (ILIT) or a Revocable Trust is the “better” option. The reality is that neither is universally better—and in many cases, the most effective plans use both.

Each trust is designed to solve a different problem. An ILIT is primarily a tax and asset-protection tool focused on life insurance, while a Revocable Trust is a foundational estate-planning vehicle used to manage assets, avoid probate, and maintain control during life. The right solution depends on individual goals, asset composition, and long-term planning priorities.

Because these trusts serve distinct purposes, choosing between them is less about comparison and more about alignment. Understanding how each structure works—and when it makes sense to use one or both—is essential to building an estate plan that protects wealth, maintains flexibility, and supports generational objectives.

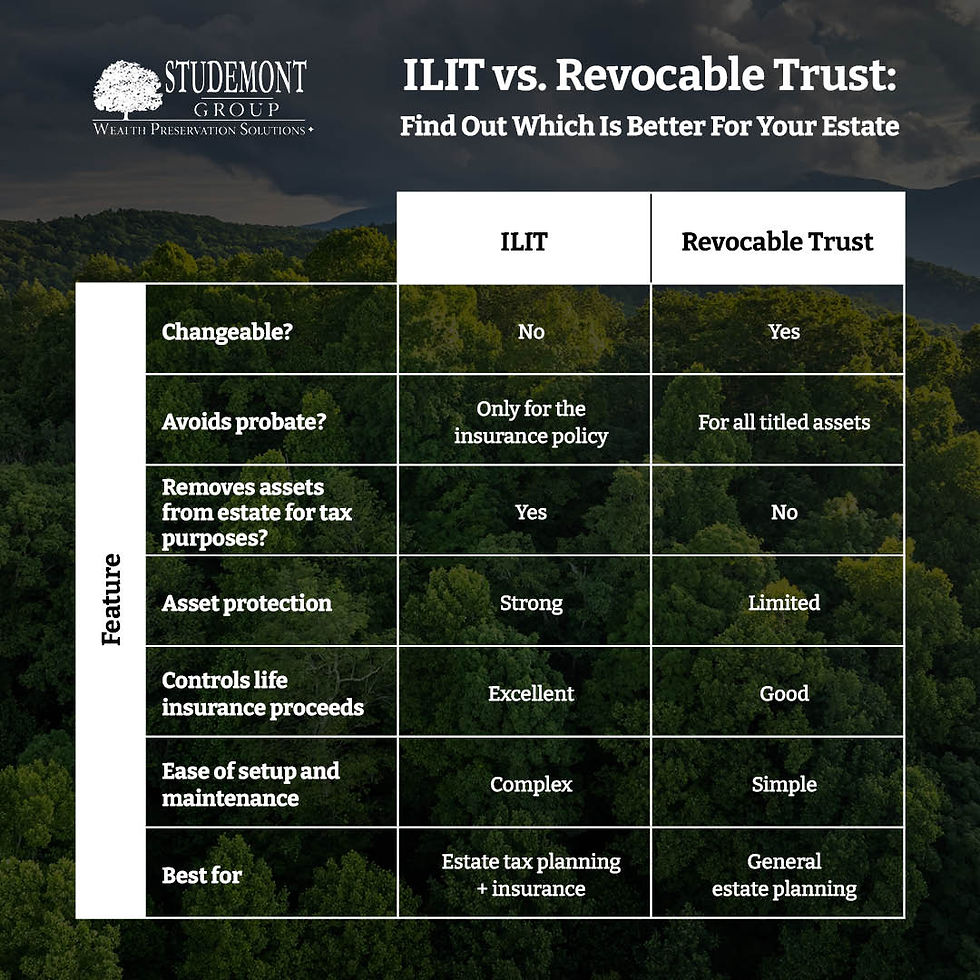

Expanding on the Short Answer

Neither an ILIT nor a Revocable Trust is inherently superior. They are designed for different functions and are often complementary. An ILIT is best suited for removing life insurance from the taxable estate and protecting proceeds from creditors or misuse. A Revocable Trust, by contrast, is most effective for avoiding probate, maintaining privacy, and providing flexible control over assets during life. In many sophisticated estate plans, a Revocable Trust serves as the primary planning vehicle, while an ILIT is used specifically to address life insurance and estate-tax exposure.

Longer Answers: What Each Trust Does

1. ILIT (Irrevocable Life Insurance Trust)

As we covered in-depth here, the purpose of an ILIT is for estate tax reduction, asset protection, and the controlled distribution of insurance proceeds.

Key Features of an ILIT

Irrevocable: You cannot change or dissolve it easily.

Owned by the trust: Life insurance is not part of your estate, it is transferred to the trust.

Shelters death benefit from estate taxes.

Can protect beneficiaries from poor financial decisions.

Is entirely run by a Trustee you appoint, not you.

Requires strict annual administration (e.g., Crummey notices) from the Trustee.

What an ILIT is Best For:

High-net-worth individuals facing estate taxes.

People who want their life insurance protected from creditors or divorcing spouses.

Ensuring there are controlled payouts (e.g., for young children).

2. Revocable Living Trust

The purpose of a revocable living trust is different. It is most commonly used for probate avoidance, privacy, smooth wealth transfer, and lifetime control for you instead of a Trustee.

Key Features of a Revocable Trust:

Revocable — You can change or cancel it.

You control the assets instead of a Trustee.

Probate is avoided for assets titled in the trust.

It offers privacy (unlike a will).

It does not reduce estate taxes.

Your assets are still reachable by your creditors.

What a Revocable Trust is Best For:

Almost anyone who prefers easy estate administration.

Blended families.

People with property in multiple states (as it avoids multiple probates).

Older adults wanting incapacity planning.

Which Is Better For You?

Choose an ILIT if:

Your estate may exceed federal or state estate tax limits.

You own large life insurance policies ($5M–$50M+).

You want to protect life insurance from creditors.

You need controlled, long-term distribution for beneficiaries.

Choose a Revocable Trust if:

You want to avoid probate.

You want full control of your assets while alive.

You want flexibility and easy updates.

You want a smooth process for your family.

Choose BOTH if:

You want comprehensive estate planning.

You have significant assets and large life insurance.

You want probate avoidance and estate-tax savings.

Many sophisticated estate plans rely on both, because they address different needs. Speak with your Estate Planning Attorney to outline what your goals are and what path works best for you to achieve them.

You should be aware that an ILIT is not a substitute for a Revocable Trust. A Revocable Trust handles your overall estate; an ILIT handles a specific asset (life insurance) for special tax and protection purposes.

When determining your goals and the best path forward, consider factors such as your approximate net worth, the size of your life insurance policies, your state of residence and applicable estate laws, your family circumstances, and your overall estate tax exposure.

Please note that Studemont Group, LP is not a legal firm and does not offer legal advice. We advise you to consult with your attorney, and we are happy to coordinate with your counsel in creating and executing your ILIT strategy.

Comments